Weekly snapshot (week ending 7 Nov 2025)

- Nifty 50: 25,492.30 (cash close on 7 Nov 2025)

- Week performance: Indices finished the week marginally lower — profit-taking and foreign flows trimmed the strong October gains; intraday volatility was noticeable.

- After Wed, 29th Sep 2025, a speedy decline in the NIFTY and all the 5 days barring one, it snapped to fresh lows and one can clearly see a weekly loss after a stretch of upside in October.

- Volatility & derivatives: India VIX rose into the mid-teens area (reported ~12.56) and Nifty November futures traded at a visible premium to cash on expiry-week flows.

Key drivers and risks

Drivers this week

- Earnings season tailwinds — pockets of positive corporate results (some big names beat estimates), which helped limit downside and supported selective sectors.

- Derivatives positioning — futures staying at a premium pointed to continued institutional hedging/positioning into month-end.

- FPIs activity — mixed flows during the week; there was meaningful FPI participation earlier in the week even as sentiment reversed late.

Risks

- Foreign outflows / global rates narrative — worries around delayed US rate cuts and global inflation dynamics dented risk appetite and prompted profit-taking.

- Event risk / geopolitics & trade talks — ongoing headlines around international trade negotiations, repeated uncertainty regarding Indo-US tariff negotiations and corporate stake sales (eg. large stake transactions/discounted sales) created general weakness in sentiments and stock-specific volatility.

- Macro prints (inflation / FX) — INR drift and any surprise macro numbers (FX reserves) could re-rate markets quickly; rupee was broadly flat-to-weak on Friday which keeps import-sensitive sectors watchful.

Fundamental view

- Earnings vs. valuations: The ongoing earnings season has delivered mixed outcomes — several large caps reported beat/upgrade momentum while a subset of cyclical and discretionary names disappointed, prompting selective rotation. That keeps the fundamental picture heterogeneous: corporate profits are broadly improving, but valuations on some large-cap pockets remain rich versus growth prospects.

- Flow backdrop: Foreign Institutional investors have been a swing factor — some weeks showing net buying but headline sensitivity around US policy and global risk means flows can reverse quickly. Long-term investors should watch FII trends and domestic institutional activity for confirmation of any sustainable move.

Technical view

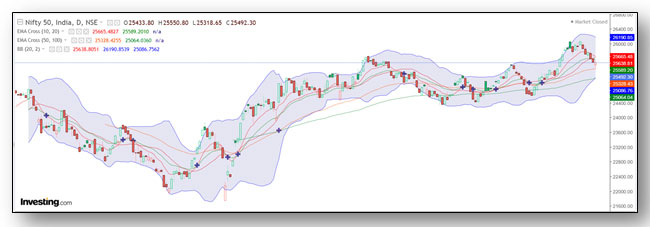

- Index structure: Nifty consolidated around 25,400–25,750 during the week, with a close at 25,492.3 on 7 Nov — indicative of a short-term pause after October gains. Support showed up near prior demand zones in the mid-25,000s while immediate resistance remains around prior highs near 25,750–25,900.

NIFTY took support at the 50EMA of 25,328 (actually went down to 25,318) before closing higher at 25,492 – momentum indicators still showing weakness at these levels - Breadth & sectors: Market breadth weakened on Friday with defensive/commodity pockets outperforming at times; midcaps showed relative weakness on profit-taking days. Stocks with recent run-ups were the hardest hit on intraday reversals.

- Sentiment indicators: India VIX ticked up (reported ~12.56) and futures were trading at a premium — a short-term signal of elevated hedging and cautious sentiment among participants.

Outlook for the coming week (10–14 Nov 2025)

- Base case (most likely): Consolidation with selective upside. Expect sideways-to-mildly-positive trade if global rates stabilize and FII flows turn neutral-to-positive. Market may rotate into structurally strong large caps (financials, select IT, defensive consumer names) while cyclicals wait for clearer macro cues.

- Bull case: A dovish Fed signal, plus continued strong domestic earnings, could trigger fresh buying and push Nifty back into positive territory

- Bear case: Renewed FII outflows or surprising hawkish global data could extend profit-taking; break below the mid-25,000s would likely accelerate the correction toward the 24,500–25,000 area.

What should retail investors do

- Keep cash/flex exposure for selective entry on pullbacks into clear demand zones.

- Deploy resources smartly into maintaining a diversified portfolio and spread your risk thin so that one can have a broad exposure to good fundamentally strong names

- Prefer quality names with strong balance sheets and visible earnings upgrades

- Avoid chasing momentum names that already extended strongly in October.